Lending to friends and relatives is a tricky business, and not only because of the stress it can place on your relationships. There are tax issues involved as well. If you have to lend money to someone close, here are some tips to do it right in the eyes of the tax code.

Charge Interest, Even to Friends and Family

Yes, you should charge interest, even to friends and family. If you don’t charge a minimum rate, the IRS will imply interest in the loan and tax you for the interest they assume you should be getting. This can occur even if you’re not actually getting a dime.

Charge Enough Interest

Not only should you charge interest, the amount must be reasonable in the eyes of the IRS. If it’s not, the IRS will imply interest at their minimum applicable federal rates (AFRs). To stay on the safe side, always charge an interest rate at or above these AFRs, available on the IRS website. The good news is these interest rates are low and almost always below the prime interest rate.

Know the Exceptions to Interest

You might be wondering: “There’s no way around this? I don’t want to charge interest to my family.”

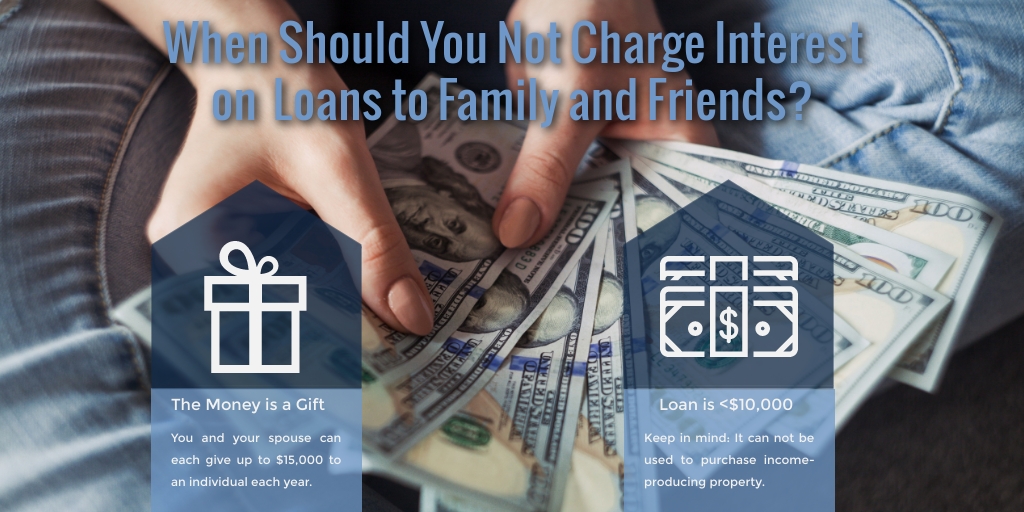

While not every situation offers exceptions, there are two for you to take note of.

Two Exceptions to Charging Interest on Loans to Family and Friends:

- The money is a gift. You and your spouse can each give up to $15,000 to an individual each year (this maximum remains $15,000 in 2019).

- The loan is less than $10,000 and is not used to purchase income-producing property.

If you don’t charge interest and the loan is used to purchase income-producing property such as capital equipment or to acquire a business, special tax rules apply. In this case it’s good to ask for assistance.

Get it in Writing

If you expect repayment, write out the terms of your loan. There are a variety of basic loan document formats online that you can use. Creating a loan document may seem unnecessarily formal when dealing with a friend or family member, but it’s important for two reasons.

1. It documents your tax code compliance. By documenting the terms and charging a stated interest rate you can clearly show you are within tax code rules.

2. You avoid misunderstandings. Creating a written document will make it clear that it is a real loan, not an informal gift. Your friend or relative will know that you expect to be paid back and when you expect repayment.